Abstract

Experimental evidence suggests that decision-making has a stochastic element and is better described through choice probabilities than preference relations. Binary choice probabilities admit a strong utility representation if there exists a utility function u such that the probability of choosing a over b is a strictly increasing function of the utility difference \(u(a) -u(b) \). Debreu (Econometrica 26(3):440–444, 1958) obtained a simple set of sufficient conditions for the existence of a strong utility representation when alternatives are drawn from a suitably rich domain. Dagsvik (Math Soc Sci 55:341–370, 2008) specialised Debreu’s result to the domain of lotteries (risky prospects) and provided axiomatic foundations for a strong utility representation in which the underlying utility function conforms to expected utility. This paper considers general mixture set domains. These include the domain of lotteries, but also the domain of Anscombe–Aumann acts: uncertain prospects in the form of state-contingent lotteries. For the risky domain, we show that one of Dagsvik’s axioms can be weakened. For the uncertain domain, we provide axiomatic foundations for a strong utility representation in which the utility function represents invariant biseparable preferences (Ghirardato et al. in J Econ Theory 118:133–173, 2004). The latter is a wide class that includes subjective expected utility, Choquet expected utility and maxmin expected utility preferences. We prove a specialised strong utility representation theorem for each of these special cases.

Similar content being viewed by others

Notes

Throughout the paper, we make the traditional Knightian distinction between a risky prospect—in which objective probabilities are attached to each possible outcome—and an uncertain (or ambiguous) one, in which outcomes are contingent on states without objective probabilities.

Hey, Lotito and Maffioletti use a Bingo Blower to generate ambiguous probabilities. This allows them to vary the ambiguity of the probabilities by varying the number and composition of balls in the blower. The relative performance of SEU actually improves as probabilities become more ambiguous—compare Treatment 1 to Treatment 3 in their Table 1.

In fact, M-linearity describes a family of properties, indexed by the set \(M\subseteq A\) on which the function must be mixture linear. Formal definitions of mixture linearity and M-linearity are given in Sect. 3.

We say that a utility function is invariant biseparable—or has the invariant biseparable form—if it represents invariant biseparable preferences; that is, has the form indicated in Theorem 11 of Ghirardato et al. (2004).

Blavatskyy’s conditions are also necessary for a strict Fechner representation (Ryan 2015), that is, a Fechner representation for P in which the utility function represents the weak stochastic preference relation \(\succsim ^{P}\). A strong Fechner representation is always strict, but the converse implication does not hold.

Dagsvik’s axioms are also necessary if choice probabilities are represented as a continuous and strictly increasing function of utility differences.

Axiom D5\(^{*} \) in Dagsvik (2015) is a weaker variant.

Suppose \(A=\left\{ a,b,c\right\} \) and there is probability \(\frac{1}{2}\) of drawing a utility function with \(u(b)>u\left( c\right) >u(a) \) and probability \(\frac{1}{2}\) of drawing a utility function with \( u\left( c\right)>u(a) >u(b) \). Then \(a\succsim ^{P}b \) and \(b\succsim ^{P}c\) but \(c\succ ^{P}a\).

Terminology in this area exhibits some variation. Debreu (1958) says that u is a “utility” for P when (6) is satisfied for any \(a,b,c,d\in A\). Luce and Suppes (1965) call u a “strong utility” if (6) holds whenever \(P(a,b) \in \left( 0,1\right) \) and \(P\left( c,d\right) \in \left( 0,1\right) \).

There is a closely related literature in which the primitive P is replaced by a weak order \({\hat{\succsim }}\) on \(A\times A\), called a difference relation, and sufficient conditions are sought for a utility-difference representation:

$$\begin{aligned} (a,b) {\hat{\succsim }}\left( c,d\right) ~~~\Leftrightarrow ~~~u(a) -u(b) \ge u\left( c\right) -u(d) \text {.} \end{aligned}$$The paper by Köbberling (2006) is in this tradition and also gives a useful summary of the previous literature.

However, the plausibility of certain axioms may.

Köbberling (2006) introduces a related, but weaker, condition that she also calls solvability.

Dagsvik defines Strong Independence for \(A=\varDelta ^{n}\), but it is clearly meaningful for any mixture set. We interpret it in this broader sense throughout the paper.

Our own proofs do not follow this recipe directly, since doing so often introduces redundancy in the set of axioms obtained. The axioms added at Step 3 may allow some of the axioms constructed in Step 2 to be weakened or removed.

Compare Dagsvik (2008, Theorem 1).

They also tested three non-preference-based models of choice, all of which performed very badly, and decision field theory, which is a type of random SEU model. Decision field theory exhibited fair-to-middling performance.

For comparison, the utility models were also embedded in the context-dependent Fechner structure proposed by Wilcox (2008). The SEU model performed slightly better in this context-dependent structure than in the conventional strong utility formulation.

See Gilboa and Schmeidler (1989).

Recall that \(0\in \mathrm {int}\left( \varSigma \right) \).

We could also have applied Proposition 1 to deduce this directly.

Here is a sketch. First, extend h to \({\mathbb {R}}^{S}\) by defining

$$\begin{aligned} h(x) =\ \frac{1}{\mu } h\left( \mu x\right) \end{aligned}$$for any \(\mu \in \left( 0,1\right] \) such that \(\mu x\in \varSigma ^{S}\). (Recall that 0 is in the interior of \(\varSigma \).) It can be verified that this extension is well defined and preserves all the relevant properties of h. One may easily show that the extended function satisfies the following for all \(a\in {\mathbb {R}}\) and all \(x,y\in {\mathbb {R}}^{S}\): \(h\left( ax\right) =ah(x) \) and \(h\left( x+y\right) =h(x) +h\left( y\right) \).

Grant and Polak (2013, Theorem 1 and Corollary (f)) provide an analogous result.

In (34) we treat x as a function from \({\mathcal {S}}\) to \(\varSigma \) rather than a vector.

Note that \(b\lambda c\succ ^{P}a\lambda c\) is ruled out by (35) and \(a\succ ^{P}b\).

Recall that \(a\succ ^{P}b\), so \(a\ne b\).

Let \({\hat{a}}=a\lambda c\) and \({\hat{b}}=b\lambda c\). The points x and y are chosen such that \(a=x\gamma {\hat{a}}\) and \(b=y\gamma {\hat{b}}\) for some \( \gamma \in \left( 0,1\right) \). The independence property (35) implies that \(u\left( \left( {\hat{a}}\mu {\hat{b}}\right) \gamma \left( x\eta y\right) \right) \) is constant in \(\mu \in \left[ 0,1 \right] \) for any \(\eta \in \left[ 0,1\right] \).

References

Abdellaoui, M., Klibanoff, P., Placido, L.: Experiments on compound risk in relation to simple risk and to ambiguity. Manag. Sci. 61(6), 1306–1322 (2016)

Anscombe, F.J., Aumann, R.J.: A definition of subjective probability. Ann. Math. Stat. 34, 199–205 (1963)

Binmore, K., Stewart, L., Voorhoeve, A.: How much ambiguity aversion? Finding indifferences between Ellsberg’s risky and ambiguous bets. J. Risk Uncertain. 45, 215–238 (2012)

Blavatskyy, P.: Stochastic utility theorem. J. Math. Econ. 44, 1049–1056 (2008)

Blavatskyy, P.: A model of probabilistic choice satisfying first-order stochastic dominance. Manag. Sci. 57(3), 542–548 (2011)

Blavatskyy, P.: Probabilistic subjective expected utility. J. Math. Econ. 47, 47–50 (2012)

Buschena, D., Zilberman, D.: Generalized expected utility, heteroscedastic error, and path dependence in risky choice. J. Risk Uncertain. 20(1), 67–88 (2000)

Dagsvik, J.K.: Axiomatization of stochastic models for choice under uncertainty. Math. Soc. Sci. 55, 341–370 (2008)

Dagsvik, J.K.: Stochastic models for risky choices: a comparison of different axiomatizations. J. Math. Econ. 60, 81–88 (2015)

Davidson, D., Marschak, J.: Experimental tests of a stochastic decision theory. In: Churchman, C.W., Ratoosh, P. (eds.) Measurement: Definitions and Theories. Wiley, New York (1959)

Debreu, G.: Stochastic choice and cardinal utility. Econometrica 26(3), 440–444 (1958)

Ellsberg, D.: Risk, ambiguity, and the Savage axioms. Q. J. Econ. 75(4), 643–669 (1961)

Falmagne, J.-C.: Elements of Psychophysical Theory. Oxford University Press, New York (2002)

Fishburn, P.C.: Binary choice probabilities: on the varieties of stochastic transitivity. J. Math. Psychol. 10, 327–352 (1973)

Fisburn, P.C.: The Foundations of Expected Utility. D. Reidel Publishing, Dordrecht (1982)

Ghirardato, P., Maccheroni, F., Marinacci, M.: Differentiating ambiguity and ambiguity attitude. J. Econ. Theory 118, 133–173 (2004)

Ghirardato, P., Maccheroni, F., Marinacci, M.: Certainty Independence and the separation of utility and beliefs. J. Econ. Theory 120, 129–136 (2005)

Gilboa, I., Schmeidler, D.: Maxmin expected utility with non-unique prior. J. Math. Econ. 18, 141–153 (1989)

Grant, S., Polak, B.: Mean-dispersion preferences and constant absolute uncertainty aversion. J. Econ. Theory 148(4), 1361–1398 (2013)

Gul, F., Pesendorfer, W.: Random expected utility. Econometrica 74(1), 121–146 (2006)

Halevy, Y.: Ellsberg revisited: an experimental study. Econometrica 75(2), 503–536 (2007)

Herstein, I.N., Milnor, J.: An axiomatic approach to measurable utility. Econometrica 21, 291–297 (1953)

Hey, J.D.: Experimental investigations of errors in decision making under risk. Eur. Econ. Rev. 39, 633–640 (1995)

Hey, J.D.: Choice under uncertainty: empirical methods and experimental results. In: Machina, M.J., Kip Viscusi, W. (eds.) Handbook of the Economics of Risk and Uncertainty, vol. 1, pp. 809–850. North Holland, Oxford (2014)

Hey, J.D., Lotito, G., Maffioletti, A.: The descriptive and predictive accuracy of theories of decision making under uncertainty/ambiguity. J. Risk Uncertain. 41, 81–111 (2010)

Hollard, G., Maafi, H., Vergnaud, J.-C.: Consistent inconsistencies? Evidence from decision under risk. Theor. Decis. 80, 623–648 (2016)

Jaffray, J.Y.: Linear utility theory for belief functions. Oper. Res. Lett. 8(2), 107–112 (1989)

Köbberling, V.: Strength of preference and cardinal utility. Econ. Theory 27, 375–391 (2006)

Loomes, G.: Modelling the stochastic component of behaviour in experiments: some issues for the interpretation of data. Exp. Econ. 8(4), 301–323 (2005)

Loomes, G., Pogrebna, G.: Testing for independence while allowing for probabilistic choice. J. Risk Uncertain. 49, 189–211 (2014)

Loomes, G., Pogrebna, G.: Do preference reversals disappear when we allow for probabilistic choice? University of Warwick, WMG Service Systems Research Group WP 08/15 (forthcoming in Manage. Sci.)

Loomes, G., Sugden, R.: Testing different stochastic specifications of risky choice. Economica 65, 581–598 (1998)

Lu, J.: Random Ambiguity. Unpublished working paper, UCLA (2014)

Luce, R.D., Suppes, P.: Preference, utility and subjective probability. In: Luce, R.D., Bush, R.B., Galanter, E. (eds.) Handbook of Mathematical Psychology, vol. III. Wiley, New York (1965)

Marley, A.A.J., Regenwetter, M.: Choice, preference and utility: probabilistic and deterministic representations. In: Batchelder, W., Colonius, H., Dzhafarov, E., Myung, J. (eds.) New Handbook of Mathematical Psychology, Volume 1: Measurement and Methodology. Cambridge University Press, London (2015)

Marschak, J.: Binary Choice Constraints and Random Utility Indicators. In: Arrow, K.J., Karlin, S., Suppes, P. (eds.) Mathematical Methods in the Social Sciences. Stanford University Press, Stanford, (1960)

Rieskamp, J., Busemeyer, J., Mellers, B.: Extending the bounds of rationality: evidence and theories of preferential choice. J. Econ. Lit. 44, 631–661 (2006)

Ryan, M.J.: A strict stochastic utility theorem. Econ. Bull. 35(4), 2664–2672 (2015)

Schmeidler, D.: Integral representation without additivity. Proc. Am. Math. Soc. 97, 255–261 (1986)

Schmeidler, D.: Subjective probability and expected utility without additivity. Econometrica 57(3), 571–587 (1989)

Schmidt, U., Neugebauer, T.: Testing expected utility in the presence of errors. Econ. J. 117, 470–485 (2007)

Tversky, A., Russo, J.E.: Substitutability and similarity in binary choices. J. Math. Psychol. 6, 1–12 (1969)

Wilcox, N.T.: Stochastic models for binary discrete choice under risk: a critical primer and econometric comparison. In: Cox, J.C., Harrison, G.W. (eds.) Research in Experimental Economics: Risk Aversion in Experiments, vol. 2, pp. 197–292. Emerald, Bingley (2008)

Wilcox, N.T.: Stochastically more risk averse: a contextual theory of stochastic discrete choice under risk. J. Econom. 162(1), 89–104 (2011)

Acknowledgements

I would like to thank two anonymous referees, whose careful reading and thoughtful comments have significantly improved the paper. I have also benefitted from the comments of Simon Grant, Guillem Roig and audiences at FUR 2016 (Warwick), the 2nd Singapore Joint Economic Theory Workshop, 33rd Australasian Economic Theory Workshop (Melbourne), 6th CMSS Summer Workshop (Auckland), AUT Mathematical Sciences Symposium (Auckland), VUW Microeconomics Workshop (Wellington) and seminar participants at the University of Auckland and Singapore Management University.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix 1: Proofs

1.1 Proof of Theorem 1

In what follows we will make frequent use of the following well-known result:

Lemma 3

(Davidson and Marschak 1959) Let P be a BCPF. Then P satisfies Strong Stochastic Transitivity (Axiom 1) iff it satisfies the the following condition:

for any \(a,b,c\in A\).

Property (20) is called weak substitutability. If we replace “\(\Rightarrow \)” with “\(\Leftrightarrow \)” in (20), we obtain the substitutability condition (Tversky and Russo 1969). Weak substitutability is obviously implied by substitutability, but the converse is false (Fishburn 1973).

The next result sets the foundation for our proof of Theorem 1.

Lemma 4

Let \(M\subseteq A\) and let P satisfy Axioms 1–3. Suppose further that \(\succsim ^{P}\) has an M-linear representation \(u:A\rightarrow {\mathbb {R}}\) and let \(\varSigma =u\left( A\right) \). Then there exists a function \(\pi :\varSigma \times \varSigma \rightarrow [0,1]\) such that

for any \(a,b\in A\). Moreover, \(\pi \) satisfies the following conditions for any \(\lambda \in [0,1]\) and any \(x,y,x^{\prime },y^{\prime } ,z\in \varSigma _{u}\):

-

(i)

\(\pi \left( x,y\right) =\frac{1}{2}\) iff \(x=y\).

-

(ii)

\(\pi \left( x,y\right) +\pi \left( y,x\right) =1\).

-

(iii)

\(\pi \left( x,y\right) =\pi \left( x^{\prime } ,y^{\prime }\right) \) implies \(\pi \left( x\lambda z,y\lambda z\right) =\pi \left( x^{\prime } \lambda z,y^{\prime } \lambda z\right) \).

-

(iv)

\(\pi \) is continuous in each argument.

-

(v)

\(\pi \) is strictly increasing (respectively, strictly decreasing) in its first (respectively, second) argument.

Proof

Since u is M-linear, \(\varSigma \) is an interval in \({\mathbb {R}}\) (Lemma 2). The weak substitutability condition—which is implied by Axiom 1 (Lemma 3)—together with (3) gives

for any \(a,b,c\in A\). It follows that (21) determines a well-defined function \(\pi :\varSigma \times \varSigma \rightarrow [0,1]\). It remains to show that \(\pi \) satisfies properties (i)–(v).

Property (i) is immediate from the definition of u. Property (ii) follows from (3).

Strong M-Independence of P and the M-linearity of u imply

for any \(x,y,x^{\prime } ,y^{\prime } \in \varSigma \) and any \(z\in u\left( M\right) \). Since \(u\left( M\right) =u\left( A\right) =\varSigma \), property (iii) holds.

To establish property (iv), note that \(\pi \) inherits solvability with respect to its second argument: for any \(x,y,z\in \varSigma \) and any \(q\in \left[ 0,1\right] \), if \(\pi \left( z,x\right) \ge q\ge \pi \left( z,y\right) \) then \(\pi \left( z,w\right) =q\) for some \(w\in \varSigma \). The weak substitutability property, together with (ii), implies that \(\pi \) is also non-increasing in its second argument. It follows that \(\pi \) is continuous in its second argument. Continuity in its first argument therefore follows from (ii).

As already noted, Strong Stochastic Transitivity (Axiom 1) implies that \(\pi \) is non-increasing in its second argument. Suppose, contrary to what we need to show, that \(\pi \left( x,y^{0}\right) =\pi \left( x,y^{1}\right) \) for some \(y^{1}>y^{0}\). We can exclude the possibility that \(x\in \left[ y^{0},y^{1}\right] \) since (i) and weak monotonicity would then imply \(\pi \left( x,y^{0}\right) <\pi \left( x,y^{1}\right) \). Hence, either \(x>y^{1}>y^{0}\) or \(y^{1}>y^{0}>x\). We only consider the former case, since the latter may be handled similarly. Thus:

Let \(\lambda \in \left( 0,1\right) \) satisfy \(y^{1}=y^{0}\lambda x\) and define \(y^{n}=y^{n-1}\lambda x=y^{0}\lambda ^{n}x\) for each \(n\in \left\{ 2,3,\ldots \right\} \). Since \(\pi \left( x,y^{0}\right) =\pi \left( x,y^{1}\right) \), property (iii) gives \(\pi \left( x,y^{0}\right) =\pi \left( x,y^{n}\right) \) for all n. By continuity

which contradicts (22). This proves that \(\pi \) is strictly decreasing in its second argument. Using (ii), we deduce that it is also strictly increasing in its first argument. \(\square \)

Corollary 2

Let \(M\subseteq A\) and let P satisfy Axioms 1–3. If there is an M-linear utility representation for \( \succsim ^{P}\), then P satisfies the substitutability property; that is,

for any \(a,b,c\in A\).

Proof

Strong Stochastic Transitivity (Axiom 1) implies the “only if” part of (23)—recall Lemma 3. The “if” part follows from property (v) in Lemma 4. \(\square \)

Before proving Theorem 1, let us outline the main obstacle to be overcome. Suppose P satisfies Axioms 1–2 and Strong M-Independence, and suppose further that u is an M-linear representation for \(\succsim ^{P}\). Consider the weak order \(\ge ^{*} \) on \(\varSigma \times \varSigma \) represented by the function \(\pi \) defined in Lemma 4:

If we can show that \(\ge ^{*} \) has a linear representation, then properties (i) and (v) in Lemma 1 imply that \(\pi \left( x,y\right) =F\left( x-y\right) \) for some strictly increasing function F. This gives the desired strong utility representation for P. Establishing the existence of a linear representation for \(\ge ^{*} \) is complicated by the fact that property (iii) is weaker than the usual (Anscombe–Aumann) independence condition on \(\ge ^{*} \). Property (iii) ensures only the Certainty independence (or C-independence) of \(\ge ^{*} \).Footnote 25 We must therefore use the other properties of \(\pi \) to make up for this deficiency.

Proof of Theorem 1 Suppose \(u:A\rightarrow {\mathbb {R}}\) is an M-linear representation for \(\succsim ^{P}\) with \(u\left( A\right) =u\left( M\right) =\varSigma \). Then \(\varSigma \) is an interval (Lemma 2). The result is trivial if \(\varSigma \) is a singleton so suppose otherwise. It is without loss of generality to assume that 0 is contained in the interior of \(\varSigma \)—if not, apply a suitable affine transformation to u.

Let \(\pi \) be defined as in Lemma 4 and let

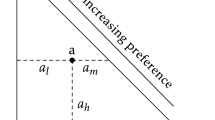

Figure 1 illustrates. Lemma 4 implies that \(\varLambda \) is the \( \pi \)-contour along which \(\pi =\frac{1}{2}\). Lemma 4 further implies that \(\pi \) is strictly increasing as we move southwards or eastwards in Fig. 1. We need to show that all the other contours of \(\pi \) are parallel to \(\varLambda \). Property (ii) ensures that these contours are symmetric about \(\varLambda \) so it suffices to consider the contours with \(\pi \left( x,y\right) <\frac{1}{2}\) (i.e. those lying above \(\varLambda \) in Fig. 1).

Suppose, contrary to what we seek to show, that there exist \(x,y,x^{\prime } ,y^{\prime } \in \varSigma \) with

but

See Fig. 1 (which assumes \(x^{\prime } >x\)).

Illustrating points (x, y) and \((x',y')\) in the proof of Theorem 1

Constructing point \((x',y'')\) in the proof of Theorem 1

By properties (i), (iv) and (v) of \(\pi \), there exists some \(y^{\prime \prime } \in \varSigma \) such that \(x^{\prime }<y^{\prime \prime } <y^{\prime } \) and \(\pi \left( x,y\right) =\pi \left( x^{\prime } ,y^{\prime \prime } \right) \). Since \(\left( x^{\prime },y^{\prime \prime } \right) \) lies below the line segment joining \(\left( x,y\right) \) to \(\left( x^{\prime } ,y^{\prime } \right) \), we must have

for some \(z\in {\mathbb {R}}\) and some \(\lambda \in \left( 0,1\right) \). Figure 2 illustrates (again for the case \(x<x^{\prime } \)). We may further assume that \(z\in \varSigma \); otherwise, we can use property (iii) to contract \( \left( x,y\right) \) and \(\left( x^{\prime },y^{\prime \prime } \right) \) towards \(\left( 0,0\right) \) until this condition is satisfied.Footnote 26

From (24) and the fact that

repeated applications of property (iii) give

Since \(\left( x\lambda ^{n}z,y\lambda ^{n}z\right) \rightarrow \left( z,z\right) \) as \(n\rightarrow \infty \) and \(\pi \left( z,z\right) =\frac{1}{2} \), we deduce a contradiction to the continuity property (iv). The contradiction is not quite immediate, as (iv) does not assert the joint continuity of \(\pi \). However, for the scenario depicted in Fig. 2 we obtain the required contradiction by considering the sequence \(\left\{ \left( x\lambda ^{n}z,\ z\right) \right\} _{n=1}^{\infty } \), which also converges to \(\left( z,z\right) \) and satisfies

for all n by property (v). For the alternative scenario in which \(x>x^{\prime } \), we may consider the sequence \(\left\{ \left( z,y\lambda ^{n}z\right) \right\} _{n=1}^{\infty } \) instead.

This contradiction establishes that \(\pi \left( x,y\right) =\pi \left( x^{\prime } ,y^{\prime } \right) \) whenever \(x-y=x^{\prime }-y^{\prime } \). Since \(\pi \left( x,y\right) \) is strictly increasing in \(x-y\) by property (v), it follows that \(\pi \left( x,y\right) =F\left( x-y\right) \) for some strictly increasing function F. \(\square \)

1.2 Proof of Corollary 1

The proof of Theorem 1 establishes that \(P(a,b) =F\left( u(a) -u(b) \right) \) for some strictly increasing F—see the discussion following the proof of Lemma 4. Property (iv) in Lemma 4 ensures that F is continuous. We can obviously construct a continuous extension of F to I that is non-decreasing everywhere, satisfies \(F(x) +F\left( -x\right) =1\) for all \(x\in I\), and whose limit is 1 approaching the right-hand end of I. This will be the distribution function for a random variable with the required properties.

1.3 Proof of Proposition 1

Suppose P satisfies Axioms 1, 4 and Strong Independence. By Theorem 1, it suffices to prove that \(\succsim ^{P}\) has a mixture linear (i.e. A-linear) representation. We do so by showing that it satisfies the conditions of Theorem 1 in Fishburn (Fisburn 1982, Chapter 2).

It is obvious that \(\succsim ^{P}\) is complete. It is transitive by virtue of the Strong Stochastic Transitivity of P (Axiom 1). Setting \( c=d\) in the definition of Strong A-Independence, we see that \(\succsim ^{P} \) inherits the following independence property: for all \(a,b,e\in A\) and all \(\lambda \in \left( 0,1\right) \)

The proof is completed by showing that

and

are closed for any \(a,b,c\in A\).

Fix some \(a,b,c\in A\) and consider the set

It is without loss of generality to assume \(a\succsim ^{P}b\). Then \(a\lambda b\succsim ^{P}b\) for any \(\lambda \in \left( 0,1\right) \) by (26). Hence, applying (26) once more, we have:

for any \(\mu \in \left( 0,1\right) \). Since \(b\mu \left( a\lambda b\right) =a \left[ \lambda \left( 1-\mu \right) \right] b\), it follows that if \(\lambda \) is in (27) then so is any \(\lambda ^{\prime } <\lambda \). It remains to exclude the possibility that (27) is of the form \(\left[ 0,\zeta \right) \) for some \(\zeta >0\).

Let \(\left\{ \lambda _{m}\right\} _{m=1}^{\infty } \subseteq \left[ 0,\zeta \right) \) be a convergent sequence with limit \(\zeta \). Suppose \(a\lambda _{m}b\succsim ^{P}c\) for each m, while \(c\succ ^{P}a\zeta b\). Then

for each m. Let

Given some \(m\in \left\{ 1,2,\ldots \right\} \), Mixture Solvability (Axiom 4) ensures that there exists \(\mu \in \left( 0,1\right) \) such that

Since \(\mu \zeta +\left( 1-\mu \right) \lambda _{m}\in \left[ 0,\zeta \right) \) and \(\rho >\frac{1}{2}\) we have the desired contradiction.

The same argument (mutatis mutandis) shows that the set

is closed. This completes the proof of Proposition 1.

1.4 Proof of Proposition 2

Lemma 5

Suppose that P satisfies Axioms 1, 4 and 7. Then for every \(a\in A\) there exists some \( {\overline{a}}\in {\overline{A}}\) such that \(a\sim ^{P}{\overline{a}}\).

Proof

Given Strong Stochastic Transitivity (Axiom 1), the binary relation \(\succsim ^{P}\) weakly orders the elements of

Suppose that \(s^{\prime } ,s^{\prime \prime } \in {\mathcal {S}}\) are such that \( a\left( s^{\prime \prime } \right) \succsim ^{P}a(s) \succsim ^{P}a\left( s^{\prime } \right) \) for all \(s\in {\mathcal {S}}\). Then Stochastic Monotonicity (Axiom 7) implies \(a\left( s^{\prime \prime } \right) \succsim ^{P}a\succsim ^{P}a\left( s^{\prime } \right) \). That is:

Hence, Mixture Solvability (Axiom 4) ensures that

for some \(\lambda \in \left[ 0,1\right] \). \(\square \)

When P satisfies Axioms 1, 4 and 7, we may therefore associate each non-constant act \(a\in A\diagdown {\overline{A}}\) with a specific (but arbitrarily chosen) certainty equivalent, denoted by \({\overline{a}}\). For every constant act \(a\in {\overline{A}}\), we define \({\overline{a}}=a\). Hence, \({\overline{a}}\in {\overline{A}}\) and \(a\sim ^{P}{\overline{a}}\) for every \(a\in A\).

Proof of Proposition 2

The restriction of P to \({\overline{A}}\times {\overline{A}}\) satisfies Strong Stochastic Transitivity, Mixture Solvability and Strong \({\overline{A}}\)-Independence. By Proposition 1, there exists a mixture linear function \(v: {\overline{A}}\rightarrow {\mathbb {R}}\) such that

In particular, v represents \(\succsim ^{P}\) on \({\overline{A}}\). Let u extend v to A by using Lemma 5 to define \(u(a) =v\left( {\overline{a}}\right) \) for all \(a\in A\diagdown {\overline{A}} \). Then u represents \(\succsim ^{P}\) by construction. We next show that u is \({\overline{A}}\)-linear.

Suppose \(a\in A, x\in {\overline{A}}\) and \(\lambda \in \left( 0,1\right) \). Since \(P\left( a,{\overline{a}}\right) =\frac{1}{2}\), Strong \({\overline{A}}\) -Independence implies that \(P\left( a\lambda x,{\overline{a}}\lambda x\right) = \frac{1}{2}\). Thus:

where the penultimate equality uses the fact that \(v:{\overline{A}}\rightarrow {\mathbb {R}}\) is mixture linear. This proves that u is \({\overline{A}}\) -linear.

Applying Corollary 2 (with \(M={\overline{A}}\)), and making use of (3), it follows that

Combining (28) and (29), we see that u is a strong utility for P.

It remains to show that u is of the invariant biseparable class.

Observe that v and u have the same range by Lemma 5. Call this common range \(\varSigma \). Since v is mixture linear, \(\varSigma \) is an interval in \({\mathbb {R}}\) (Lemma 2). Using Stochastic Monotonicity (Axiom 7), it is easy to see that there exists a well-defined function \(h:\varSigma ^{S}\rightarrow \varSigma \) such that

for all \(a\in A\). That is, the utility of any act depends only on the v-utility obtained in each state and is uniquely determined by these v-utilities. We use h to denote the function that converts vectors of state-(v-)utilities into the (u-)utility of the corresponding act.

Let C denote the set of constant vectors in \(\varSigma ^{S}\), and identify elements of C with elements of \(\varSigma \) in the obvious fashion. We now observe that h has the following properties: (a) \(h\left( c\right) =c\) for all \(c\in \varSigma \); (b) h is non-decreasing in each argument by virtue of Stochastic Monotonicity; and (c) h is C-linear by virtue of the \( {\overline{A}}\)-linearity of u. In the language of Ghirardato et al. (2005), h is normalised, monotonic and constant affine. If P is non-trivial, then \(\varSigma \) is a non-degenerate interval and it follows (ibid., p. 132) that h has a unique extension \(h:{\mathbb {R}} ^{S}\rightarrow {\mathbb {R}}\) satisfying constant linearity: \(h\left( ax+b\right) =ah(x) +b\) for all \(x\in {\mathbb {R}}^{S}\) and all \( a,b\in {\mathbb {R}}\) with \(a\ge 0\). The desired result is now immediate from Ghirardato, Maccheroni and Marinacci (2004, Lemma 1 and Theorem 11). \(\square \)

1.5 Proof of Proposition 3

Let v and u be defined as in the proof of Proposition 2 and let h: \(\varSigma ^{S}\rightarrow \varSigma \) be the function defined by (30). Non-triviality of P implies that \(\varSigma \) is a non-degenerate interval (Lemma 2), which we assume, without loss of generality, to contain \(\left[ -1,1\right] \).

We first show that Strong A-Independence of P implies A-linearity of u. Let \(a,b\in A\) and \(\lambda \in \left( 0,1\right) \). Since \(P\left( a, {\overline{a}}\right) =\frac{1}{2}\) we deduce that \(P\left( a\lambda b, {\overline{a}}\lambda b\right) =\frac{1}{2}\) from Strong A-Independence. Thus, \(u\left( a\lambda b\right) =u\left( {\overline{a}}\lambda b\right) \). Using the \({\overline{A}}\)-linearity of u, we have:

Hence, u is A-linear.Footnote 27

Next, we show that h is mixture linear. Let \(a,b\in A\) and \(\lambda \in \left[ 0,1\right] \). If \(x_{s}=v\left( a(s) \right) \) and \( y_{s}=v\left( b(s) \right) \), then \(u(a) =h(x) \) and \(u(b) =h\left( y\right) \). Using the \({\overline{A}} \)-linearity of v and the A-linearity of u we have:

Hence, h is mixture linear. It has a unique linear extension h: \({\mathbb {R}} ^{S}\rightarrow {\mathbb {R}}\) by standard arguments.Footnote 28 Stochastic Monotonicity (Axiom 7) implies that the coefficients of this linear function are non-negative. Since u is non-constant, at least one coefficient is strictly positive so the vector of coefficients can be positively scaled to lie in \(\varTheta \). \(\square \)

1.6 Proof of Proposition 4

Once again, let v and u be defined as in the proof of Proposition 2 and let \(h:\varSigma ^{S}\rightarrow \varSigma \) be the function defined by (30).

From Stochastic Uncertainty Aversion (Axiom 8) and the \({\overline{A}}\)-linearity of v, we see that \(h:\varSigma ^{S}\rightarrow \varSigma \) satisfies—in addition to the properties noted in the proof of Proposition 2—the following: for any \(x,y\in \varSigma ^{S}\),

Its unique constant-linear extension h: \({\mathbb {R}}^{S}\rightarrow {\mathbb {R}}\) is therefore superadditive: that is,

for any \(x,y\in {\mathbb {R}}^{S}\). To see why, let \(x,y\in {\mathbb {R}}^{S}\), \( {\overline{x}}=h(x) \), \({\overline{y}}=h\left( y\right) \) and \( \varepsilon ={\overline{x}}-{\overline{y}}\). Then constant linearity and (31) give

which implies (32).

The proof is completed by applying the following well-known result (see, for example, Lemma 3.5 in Gilboa and Schmeidler 1989):

Lemma 6

Let \(h:{\mathbb {R}}^{S}\rightarrow {\mathbb {R}}\) be a superadditive, constant-linear function that is non-decreasing in each argument. Then there exists a closed and convex set \({\mathcal {P}}\subseteq \varTheta \) such that

for every \(x\in {\mathbb {R}}^{S}\).

1.7 Proof of Proposition 5

As usual, we let v and u be defined as in the proof of Proposition 2 and let \(h:\varSigma ^{S}\rightarrow \varSigma \) be the function defined by (30). Since \(\varSigma \) is a non-degenerate interval we may assume, without loss of generality, that it contains \(\left[ -1,1\right] \).

Definition 6

Vectors \(x,y\in \varSigma ^{S}\) are comonotonic if there do not exist \(s,s^{\prime } \in {\mathcal {S}}\) with \(x_{s}>x_{s^{\prime } }\) and \( y_{s^{\prime } }>y_{s}\).

If P satisfies Stochastic Comonotonic Independence (Axiom 9), then \(h:\varSigma ^{S}\rightarrow \varSigma \) satisfies

for any pairwise comonotonic \(x,y,z\in \varSigma ^{S}\) and any \(\lambda \in \left( 0,1\right) \). The desired representation is now an immediate implication of the following result:Footnote 29

Lemma 7

(Schmeidler 1986, Corollary) Let \(\varSigma \subseteq {\mathbb {R}}\) be a non-degenerate interval containing \( \left[ -1,1\right] \) and let \(h:\varSigma ^{S}\rightarrow \varSigma \) be a normalised, monotonic function that satisfies (33) for any for any pairwise comonotonic \(x,y,z\in \varSigma ^{S}\) and any \(\lambda \in \left( 0,1\right) \). Then there exists a capacity \(\omega \) such that

for all x.Footnote 30

Appendix 2: Strengthening Theorem 2

The following strengthens Theorem 2 by replacing the Quadruple Condition (Axiom 5) with Strong Stochastic Transitivity (Axiom 1).

Theorem 3

Let \(A=\varDelta ^{n}\). If P satisfies Axioms 1, 2, 6 and Strong Independence, then P has a strong utility that is mixture linear.

We use a similar argument to that for Proposition 1, except we can no longer appeal to Mixture Solvability to establish the continuity of \( \succsim ^{P}\). Instead, we show that \(\succsim ^{P}\) possesses a linear representation by an alternative route.

Proof of Theorem 3

As in the proof of Proposition 1, we may assume that \(\succsim ^{P}\) is a weak order satisfying

for all \(a,b,c\in A\) and all \(\lambda \in \left( 0,1\right) \). Since the result is obvious if \(\succsim ^{P}\) is trivial (i.e. \(a\sim ^{P}b\) for all \(a,b\in A\)), let us assume otherwise. From Axiom 6, we also know that \(\succsim ^{P}\) satisfies the following Archimedean property: for any \( a,b,c\in A\)

for some \(\lambda ,\mu \in \left( 0,1\right) \). It therefore suffices (Fisburn 1982, Chapter 2) to establish that

for all \(a,b,c\in A\) and all \(\lambda \in \left( 0,1\right) \).

Lemma 8

Condition (37) holds on the interior of A (that is, for any \(a,b,c\in A\cap {\mathbb {R}}_{++}^{n}\)).

Proof

Suppose \(a,b,c\in A\cap {\mathbb {R}}_{++}^{n}\) with \(a\succ ^{P}b\) and \( a\lambda c\sim ^{P}b\lambda c\).Footnote 31 That is,

We claim that

for any \(d,e\in A\). To see why, observe that Strong Independence and

give

The reverse inequality follows by applying Strong Independence to \(P(a,b) \ge P\left( d,e\right) \) and using (38).

We next show that \(d=a\mu b\) and \(e=b\) satisfy the antecedent in (39) for any \(\mu \in \left[ 0,1\right] \). The cases \(\mu \in \left\{ 0,1\right\} \) are trivial so we focus on \(\mu \in \left( 0,1\right) \).

Since

we have

and

by Strong Independence. From the latter inequality and weak substitutability (which is implied by Strong Stochastic Transitivity—Lemma 3), we have

for any \(\mu \in \left[ 0,1\right] \).

From (42) we obtain a linear segment of strictly positive length,Footnote 32 parallel to the line joining a and b, which forms part of an indifference curve for \(\succsim ^{P}\). Since a and b are in the interior of the simplex, we can use the existence of this linear segment, together with transitivity of \(\succsim ^{P}\) and the independence property (35), to deduce that the line segment joining a and b must also be part of an indifference curve. Figure 3 illustrates the required construction (for the case \(n=3\)). By moving point z along the segment from x to y, we sweep out an indifference curve joining a to b.Footnote 33 This is the desired contradiction, since \(a\succ ^{P}b\). \(\square \)

Since \(A\cap {\mathbb {R}}_{++}^{n}\) is a mixture set (under the usual mixing operation for \({\mathbb {R}}^{n}\)), it follows that \(\succsim ^{P}\) possesses a linear representation on \(A\cap {\mathbb {R}}_{++}^{n}\). Let u be such a representation.

Illustrating the construction in the proof of Lemma 8

Observe that Axiom 6 is not required for the proof of Lemma 8—Strong Independence does all the work. We now use Axiom 6 to extend the linear representation to the boundary of the simplex.

First, u has a unique mixture linear extension to A. We use u to denote the extended function, as no confusion should arise. Let a be a boundary point of A. There are two possibilities: either (i) \(u(a) =u(b) \) for some \(b\in A\cap {\mathbb {R}}_{++}^{n}\) or else (ii) the face of the simplex containing a is part of a contour of u.

For case (i) we show that \(a\sim ^{P}b\). (It follows that \(a\sim ^{P}b\) for any boundary point a and any interior point b on the same utility contour as a.) If, for example, \(a\succ ^{P}b\), then we can find some \(c\in A\cap {\mathbb {R}}_{++}^{n}\) with \(u\left( c\right) <u(b) =u(a) \). Hence \(a\succ ^{P}b\succ ^{P}c\), but \(u\left( a\lambda c\right) <u(b) \) for all \(\lambda \in \left( 0,1\right) \) by the mixture linearity of u. Since \(a\lambda c\in A\cap {\mathbb {R}}_{++}^{n}\) for any \( \lambda \in \left( 0,1\right) \), we have \(b\succ ^{P}a\lambda c\) for all \( \lambda \in \left( 0,1\right) \), which contradicts the Archimedean property (36). Assuming \(b\succ ^{P}a\) leads similarly to contradiction.

Now consider case (ii). Thus, u is constant on the face of the simplex containing a. Suppose, in particular, that \(u(a) >u(b) \) for all \(b\in A\cap {\mathbb {R}}_{++}^{n}\). The alternative scenario, in which \(u(a) <u(b) \) for all \(b\in A\cap {\mathbb {R}}_{++}^{n}\), may be handled similarly. We will show that \(a\sim ^{P}b\) for any b on the same face as a, and \(a\succ ^{P}b\) for any \(b\in A\) not contained in the face containing a. Combined with case (i), this shows that \(\succsim ^{P}\) is represented by u on all of A.

Suppose \(b\in A\) with \(u(a) =u(b) \), so b lies on the same face of the simplex as a. If \(a\succ ^{P}b\) then \(a\succ ^{P}b\succ ^{P}c\) for any \(c\in A\cap {\mathbb {R}}_{++}^{n}\). Since \(b\succ ^{P}a\lambda c\in A\cap {\mathbb {R}}_{++}^{n}\) for any \(\lambda \in \left( 0,1\right) \), we deduce a contradiction to (36). Assuming \(b\succ ^{P}a\) leads similarly to contradiction.

Finally, let \(b\in A\) with \(u(a) >u(b) \). Assume, contrary to what we seek to show, that \(b\succsim ^{P}a\). Since \(u(a) >u(b) \) we may choose some \(c,d\in A\cap {\mathbb {R}} _{++}^{n}\) with

Therefore, \(d\succ ^{P}c\succ ^{P}b\succsim ^{P}a\) and

It follows that \(d\lambda a\succ ^{P}c\) for all \(\lambda \in \left( 0,1\right) \). This contradicts the Archimedean property (36) and completes the proof of Theorem 3. \(\square \)

Rights and permissions

About this article

Cite this article

Ryan, M. Uncertainty and binary stochastic choice. Econ Theory 65, 629–662 (2018). https://doi.org/10.1007/s00199-017-1033-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00199-017-1033-4